Depending on the mortgage product, you may have the option to choose how frequent you can make mortgage payments. What are the options and what is the difference?

Let's review some of the common payment options and learn the basics. For the full explanations on each, you should always consult with a mortgage professional.

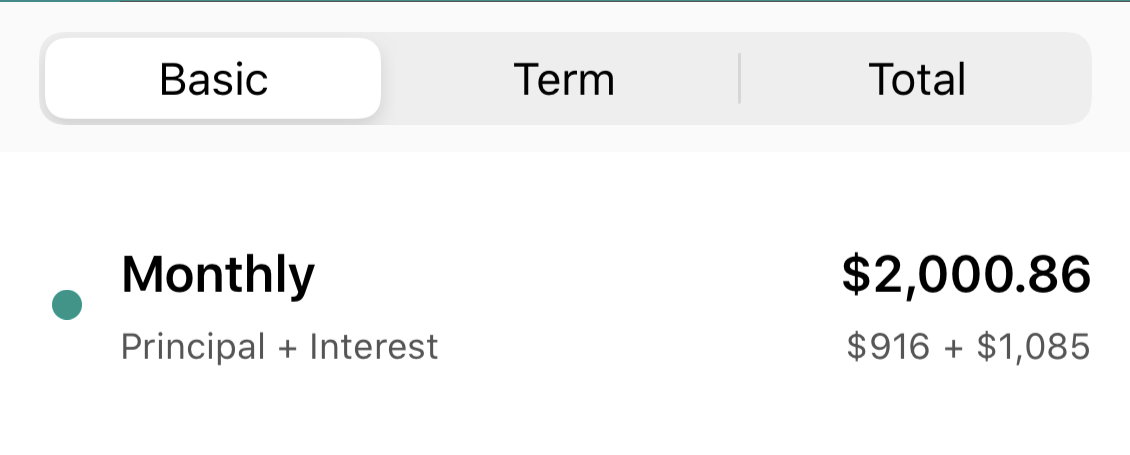

Here is how it looks on the app when Monthly is selected

Just as the name suggests, mortgage payments are due once every month. In a year, you make exactly 12 payments.

Mortgage payments are due every other week. Since it's every other week, you are making a total of 26 payment per year. A year has 52 weeks, so 52 / 2 = 26 and if you were to sum up the total payment amount in a year, it would equal to the Monthly option. You just get a tiny bit of saving because you make more frequent payments.

Accelerated Bi-Weekly also known as "Rapid". This option is awesome because it allows you to save more interest. The way accelerated works is that you pay half of the monthly amount every other week. Half of anything 26 times means that it's equal to 13 full payments. So technically, you pay 1 extra monthly payment. This option also allows you to save on time it takes to pay down your mortgage.

Now, if you were to use your finger and swipe from "Basic" To "Term", you can see more details for each payment option.

- How much interest is charged over the term of the mortgage (the term is the length of the contract you have with the lender)

- In accelerated options you can see Interest savings over the term (Term Savings)

- How much of your mortgage is paid during the term (Principal Paid)

- And finally, what is the mortgage amount going to be when the term is done. (End of Term Balance)

If you have any questions on how to use these features, let us know by tapping on the Contact Us button above.

Happy Number Crunching